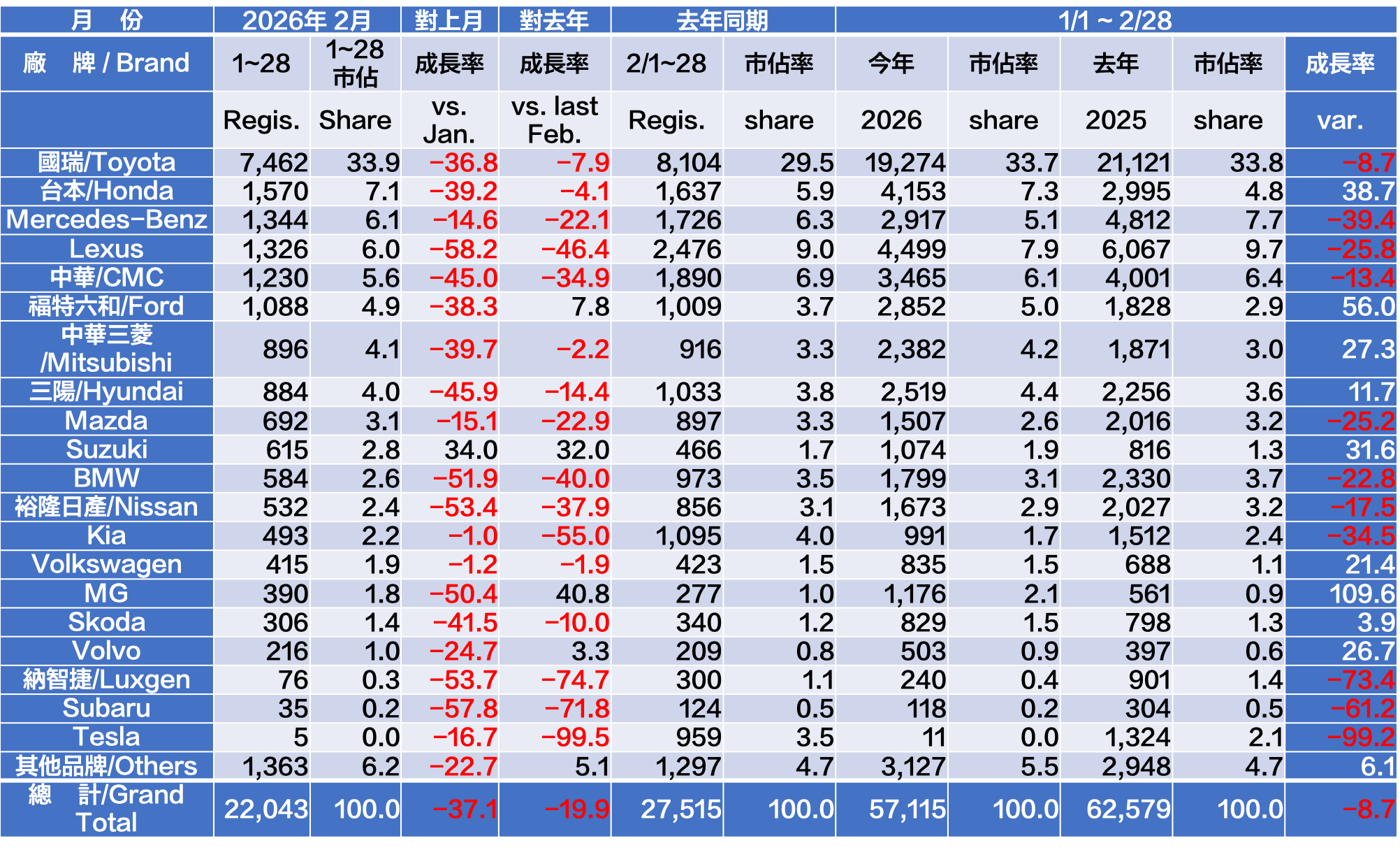

Market Overview:

As nine days of February fell within the Lunar New Year holiday period, and the month-end also coincided with the 228 Peace Memorial Day long weekend, coupled with the fact that February had the fewest available registration days of the year, total market registrations declined sharply by 37.2% compared with January, and fell 19.1% year-on-year, reaching 22,043 units. This month, all major brands recorded declines of varying degrees, with the sole exception of Suzuki, which grew by 34%. Among them, Lexus experienced the most severe decline at 58.2%, mainly because its core model lines—UX, NX, and RX—were undergoing model-year transitions, leading to reduced registrations. Of these, the UX saw the most pronounced drop, plunging by 97.1%. Cumulative registrations from January through the end of February totaled 57,116 units, representing a year-on-year decline of 8.7%. Regarding the full-year market outlook, the market leader Hotai Motor has recently projected that total sales could reach 440,000 units, implying nearly 6.2% growth compared with 2025. In our view, once the U.S. reciprocal tariff issue becomes clearer and domestic regulatory adjustments are completed, there should be room for a certain degree of price and market correction. For consumers who remained on the sidelines last year, the second half of this year is likely to be a favorable time to purchase, which could in turn help lift overall vehicle registrations and support the outlook for market growth compared with 2025.

Market share of brands:

In terms of market share this month, Toyota/Lexus continued to lead with 39%, followed by Honda in second place with 7.1%, Mercedes-Benz in third with 6.1%, CMC in fourth with 5.5%, Ford in fifth with 4.9%, Mitsubishi in sixth with 4.1%, Hyundai in seventh with 4.0%, Mazda in eighth with 3.1%, and Suzuki in ninth with 2.8%. Nearly all major brands recorded declines this month, with Suzuki being the only exception and posting growth of as much as 34%. This was mainly driven by the Swift, which recorded 352 registrations—up 343.6% from the previous month—along with a large batch of Jimny deliveries totaling 180 units.

Comparison between domestic cars and imported cars (excluding heavy duty trucks):

The sales ratio between domestic and imported vehicles this month stood at 47.2% versus 52.8%. Imported passenger vehicle sales fell sharply by 24.7% year-on-year and declined a further 28.5% compared with the previous month. The main reasons were the ongoing model-year transitions affecting imported vehicles, as well as the absence of Tesla shipments this month. Tesla, which typically accounts for a significant portion of imported vehicle sales, registered only five units, leading to a pronounced contraction in overall imported vehicle performance.

Outstanding models:

As there were only 14 working days available for vehicle registrations this month, only two models exceeded 1,000 units in sales: Corolla Cross with 2,441 units and RAV4 with 1,796 units. In the small commercial vehicle segment, J Space significantly widened its lead over Town Ace this month, registering 860 units compared with Town Ace’s 542 units. Updates to each brand’s key commercial vehicle offerings later this year are expected to be a critical factor in determining registration performance, making this segment well worth continued observation.

BEVs market:

A total of 1,464 pure electric vehicles were delivered this month, representing a sharp decline of approximately 79.6% compared with the previous month. This was mainly due to the absence of Tesla shipments, with only five in-stock Model Y and Model 3 units registered. Toyota bZ4X ranked first in the EV market this month with 438 registrations, demonstrating steady performance. Meanwhile, Foxtron’s latest domestically developed model, the Bria, recorded a total of 390 registrations. In a month with more complete sales activity, its performance is expected to reach an even more encouraging level. Other EV registrations included 76 units for the EX30 and 66 units for the n⁷. The domestic EV market contracted significantly this month due to the lack of large-scale Tesla deliveries. However, Tesla’s newly introduced Model 3 Long Range Rear-Wheel Drive variant is expected to generate strong registration numbers once shipments arrive in March. In addition, several major electric vehicle launches from traditional automakers are scheduled for later this year, including the BMW iX3, Foxtron Cavira, Hyundai Ioniq 9, Lexus ES, Mercedes-Benz CLA, Mercedes-Benz GLB, Porsche Cayenne Electric, Subaru Uncharted, Subaru e-Outback, and Volvo EX90. These models are expected to further expand the overall market share of pure electric vehicles.